The phrase is traced to Bob Hope, apparently when challenged by a heckler during one of his military morale-boosters to explain why he wasn't in uniform. “Don't you know there's a war on?” he replied. “A guy could get hurt!”

It would have been perfectly legitimate for one of the Keeneland auctioneers to respond in similar vein to the torrent of bidding that elevated the September Sale to unprecedented highwater marks. Somehow, the kind of factors that traditionally send markets into nauseous free fall have failed to stem a breathless bull run in international bloodstock. Don't these people have televisions, or newspapers?

The market's resilience through Covid was startling enough. Many of us sought to explain that by a pent-up thirst to make the most of life, after being so bleakly confined. There was also the sense that the most affluent tier of society, on which our industry so candidly depends, had been insulated from the kind of financial stress being experienced lower down the pyramid.

After all, the wealthy had benefited through the previous decade from the liquidity deployed (via cash-doping instruments such as quantitative easing) to put out the fires of the banking crisis; and those taps had never really been turned off, even after the flames abated. But now we have runaway inflation, we have the horrifying return of territorial invasion in Europe, we have ubiquitous forecasts of recession. And still the value of Thoroughbreds continues to soar.

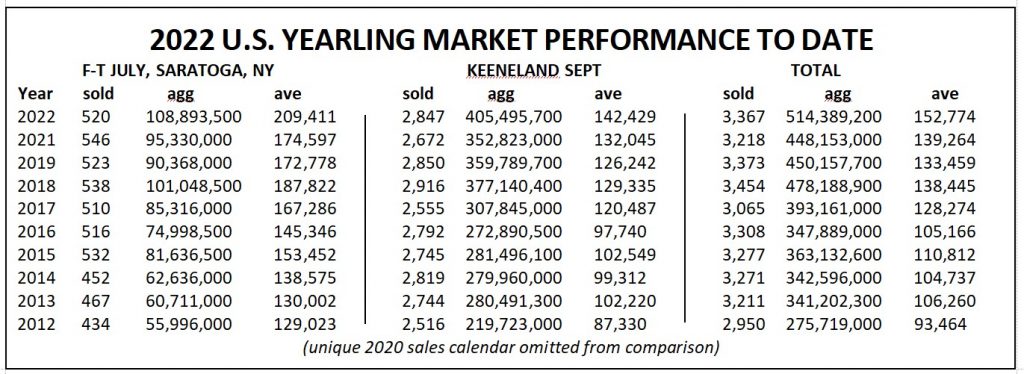

The table below shows that the average cost of a North American yearling, in 2022, has breached $150,000 in a market that has passed another historic barrier, for this stage of the calendar, at $500 million. This is calculated from aggregate business at Fasig-Tipton's three summer auctions-the July Sale in Lexington, plus the elite and New York catalogues at Saratoga-combined with turnover at Keeneland over the past two weeks, where transactions spanned $2,000 to $2.5 million. Together, as such, these comprise a comprehensive snapshot of the marketplace at all levels.

Turnover at the September Sale advanced 14.9% on last year to exceed $400 million for the first time (missed by a few cents in 2006); while the Fasig-Tipton summer calendar advanced in step by 14.2% to achieve a record aggregate of its own at nearly $109 million. Collectively, an additional $66,236,200 has been spent on North American yearlings so far this year, an increase of 14.8% to $514,389,200. That represents an 86.6% gain on the equivalent stage in 2012!

These numbers translated to record averages of $209,411 for Fasig-Tipton, up a staggering 20% on 2021; and $142,429 for Keeneland, an increase of just under eight%. Blended, the average yearling is costing you $152,774 in 2022, up $13,510 or 9.7% on this time last year.

Now a lot of this has a very edifying impetus. A number of regions, not least Kentucky itself, have been developing a purse structure that threatens to introduce something resembling coherence-even, whisper it, viability-to investment in Thoroughbreds. Nor should we forget our collective debt to those who have heroically restored the sport in California from an existential brink, renewing geographical balance to opportunity. And of course the circuit there has meanwhile produced a racehorse that has made even a seven-figure tag look cheap.

But perennial growth, in a market like this, is impossible. Capitalism has always depended on cycles, requiring troughs to generate the conditions for the next peak. Just conceivably, globalization may have so skewed the system that the elite can remain blithely immune to street-level difficulties. But if recession does end up penetrating the entire economic organ, the way it always has in the past, then we must give Cassandra her say. Because the bloodstock market has tended to absorb trends from the wider economy slowly, whether in recession or recovery.

The Dow Jones, having plunged 33.8% in 2008, recovered 18.8% as soon as the following year and maintained solid gains annually until 2015. The overall North American bloodstock market, in contrast, lost 21.2% in 2008; 32.2% in 2009; and another 6.5%, even on those compound losses, in 2010. It was not until 2011 (up 18.2%) and especially 2013 (up 27.9%, in tandem with the biggest spike in the Dow Jones) that its own recession leveled out.

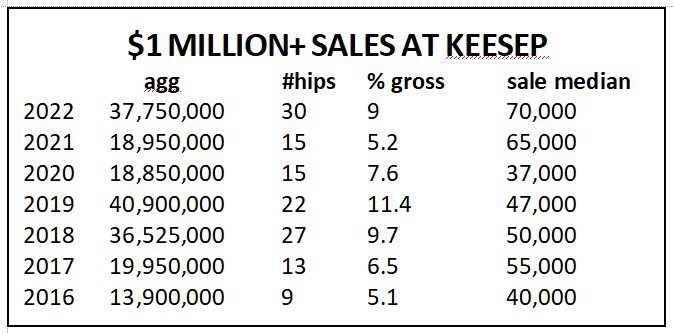

For the time being, however, we must acknowledge a wholesome depth to the current market. Vendors always complain about polarization, about a soft center and all-or-nothing engagement (often contingent on vetting). But this feels different. Among the many records set at Keeneland, perhaps the most significant was one of 82% clearance.

While 30 seven-figure sales headlined the feel-good stories at that auction, the fact is that they only narrowly surpassed the 27 recorded in 2018. In each case, moreover, their collective cost represented a very similar portion of overall turnover: nine% this year, against 9.7 per cent in 2018. (The spike to 11.4% in 2019, by the way, was largely the work of the ill-fated $8.2 million daughter of Leslie's Lady and American Pharoah). As the table below demonstrates, however, the median across the two weeks was wildly higher this year, at a record $70,000 against $50,000 in 2018.

This depth is reciprocated by the sheer breadth of investment, with no fewer than 88 different signatories to dockets together worth $1 million or more.

For years, people asked queasily what would happen to the market if deprived of support from a family that had, globally, done so much to assist the evolution of a commercial breeding industry. As recently as 2019, Godolphin and Shadwell topped the September action with an outlay of $16 million and $11.07 million respectively for a total of 28 yearlings. Since then, we have mourned the passing of Shadwell's founder Sheikh Hamdan, albeit that firm did acquire four yearlings for a total $2.5 million this year. And Sheikh Mohammed, meanwhile, has become conspicuous by his absence at this sale.

In the event, however, the defection of spenders apparently able to bid indefinitely has only cleared the field for competition. The best prospects have not become more affordable, in themselves. But they have become more accessible. As a result, competition has been intensified, not diluted, even as powerful domestic interests have increasingly collaborated in pursuit of common targets.

This September it was only by a single nod to the rostrum that the charismatic duo behind Repole Stable and St. Elias Stables edged out another powerful partnership to finish the auction once again as leading buyer: their $12,840,000 outlay (for 31 yearlings) shading Donato Lanni's $12,825,000 on behalf of SF/Starlight/Madaket. But that was barely half the story, as West Bloodstock signed as agent for Repole Stable for 27 additional head at $7,940,000; while Michael Wallace corralled 15 at $4,475,000 for St. Elias Stables. These extra investments weighed in respectively as the fourth and eighth highest of the sale; and that's besides a series of individual plays with other partners.

The latter included M.V. Magnier, whose $1.1-million Curlin colt with Repole Stable was one of a handful such investments made with partners. Magnier, representing the Maktoums' traditional antagonists at Coolmore, actually signed for only a couple of colts outright. With the strength of the dollar steepening the gradient against overseas currency, Hideyuki Mori had to settle for five head at $2,545,000, compared with a dozen at $4,415,000 in 2021. That left agent Richard Knight's dazing spree in the second session as the only really striking external contribution to the top end of the market, his total spend (#7 for the sale) comprising $4,875,000 across half a dozen hips.

So much for the joys of being able to travel freely again! In the longer view, however, what we saw is consistent with ongoing European mistrust of Kentucky sires, and the lamentable transatlantic schism between perceived dirt and turf bloodlines.

As for the corresponding local neglect of grass stallions, there was at least some belated respect for two outstanding turf stallions recently lost to the Bluegrass: English Channel tipped six figures for the second year running, after averaging no more than $33,167 only in 2020, while Kitten's Joy averaged $138,632 for 19 yearlings (up from $103,457 last year).

As anticipated from the conspicuous distribution of his stock towards the front of the catalogue, this sale proved another major landmark in the career of Quality Road. With several proven titans approaching the evening of their careers, the 16-year-old Lane's End stallion sealed his accession to that level by again keeping even champion Into Mischief (58 sold at $525,776) from the top of the averages, processing 37 at $533,514. That was a further advance on the $472,794 by which Quality Road shaded Curlin and Into Mischief in 2021, having the previous year slipstreamed Medaglia d'Oro, Into Mischief, Tapit and Curlin at $339,939.

The much younger Gun Runner meanwhile maintained his stratospheric rise, processing 40 hips at $461,875, good enough for third with yearlings still conceived off his $70,000 opening fee. (And remember that his current weanlings came into the world at $50,000! What kind of fee, you wonder, will register the upgrade in his mares guaranteed in 2023?)

As always, however, most curiosity was reserved for those newcomers who nowadays comprise the bedrock of the commercial market. Their window of opportunity is so fleeting as to make it seem almost cruel to examine their performance too closely, when really they should not be judged at all until their stock reaches the racetrack. But if that's how the market will insist on behaving, then that's how we must assess their debuts to this point.

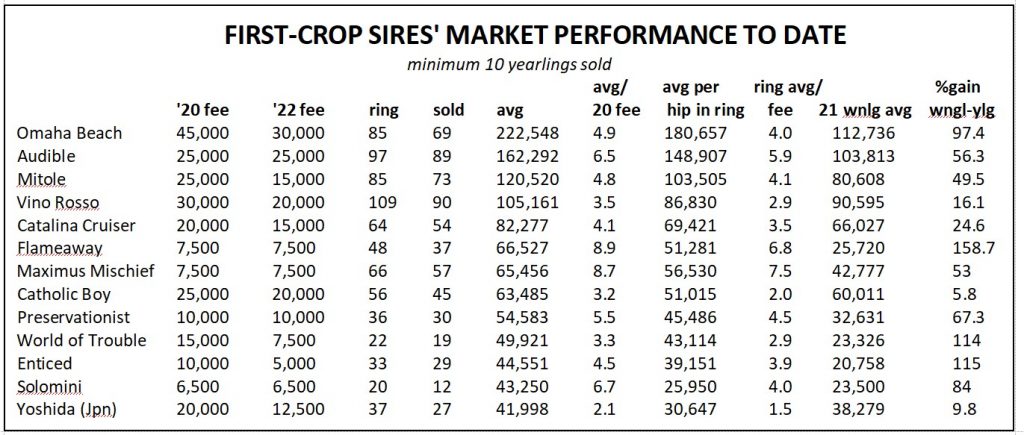

Obviously there are several auctions still to come, but the pyramid of business to date plainly provides a valid sampling. The table below charts those sires whose debut crops have so far mustered at least 10 sales.

Now some people feel it's a little strange that sires are given a pass on stock they can't sell. The difficulty is that a yearling that fails to reach its reserve will sometimes be among the very best of a sire's crop, its vendor only receptive to the kind of offer that can't be refused. Equally, however, an RNA can often reflect a simple failure of traction. Arguably data should give some credit to the sire who processes a high percentage of his stock. For the little it may be worth, then, our table also includes average revenue per hip into the ring, as an extra snapshot of how he might be working out, overall, an investment vehicle.

Because while the table is sorted according to average sales, we do know that the market tends to be pretty obedient in that respect. Year after year, first crops tend to end up being valued more or less in line with the pecking order invited by opening stud fees.

Just as well, then, that Omaha Beach has done exactly what he was priced to do, averaging five times his opening fee at $222,548. He has looked value throughout, to be fair, and has certainly been kept in the game with consecutive fee cuts since siring these yearlings. Having retained his opening fee, equally, Audible has arguably done no less than required in averaging a whopping 6.5 yield.

If these two haven't put a foot wrong, others who have not done quite so well-in what remain, after all, extremely early skirmishes-have tended to have their fees trimmed as an incentive to keep the faith. But I think one or two sires deserve a little extra attention, at this stage, if we put on the pinhooker's hat.

Again, this is an inexact exercise. Different horses are different projects. But let's take a look at the advances made by these stallions between their weanling and yearling averages, as a possible gauge of the kind of physical progress their stock can make.

Omaha Beach has excelled in this respect, certainly, essentially doubling his weanling average. But let's shine a torch at the other end of the spectrum. While cheaper stallions are obviously obliged to make pretty brisk gains just to cover keep, smaller breeders are grateful even for modest margins.

Flameaway owes his vivid climb on these indices partly to a single $425,000 colt at Saratoga, but his weanling median of $17,500 has also been hoisted at a comparable rate, to $50,000. Overall, his revenues, for sales achieved and per hip into the ring, respectively represent almost nine and seven times his fee. Darby Dan knows how to put numbers behind a cheap young stallion and perhaps Flameaway, who beat Catholic Boy and Vino Rosso on the Derby trail, will take his chance after the fashion of Dialed In. Apart from anything else, his third dam is a turf matriarch and, with his flexible sire-line, the son of Scat Daddy merits close attention from European breeze-up pinhookers seeking an export bargain.

Another who started with a very big book on the same basement fee, Maximus Mischief, achieves the highest ratio of all per hip into the ring (7.5 times his fee; also nearly nine times his fee on sales completed) after finding homes for 57 of 66 yearlings offered to date. He has added 53% to his weanling average and, with his profile, looks a blatant vehicle for the next pinhooking cycle, too.

Preservationist was unfortunate that the colt he got into Book I-a rare achievement for a $10,000 sire-had to be scratched from the September Sale. Even without his star turn, however, he achieved some outstanding dividends, including colts at $280,000, $260,000 and $250,000 deeper in the catalogue. Overall he has put two-thirds onto the average value of his weanlings, and his yearling sales are averaging 5.5 his fee. This guy offers exemplary genetic depth, remember, and don't be deceived by the hold-ups that delayed his bloom on the racetrack. He got a 31/2 Ragozin breaking his maiden over six furlongs, and the platform he has already built for himself suggests that there will be precocity to match that speed.

All these are just straws in the wind, of course, and far-sighted supporters of some that have failed to achieve gaudy overnight dividends will be wisely content to wait until actually able to test the water on the racetrack. Because there's one big problem with a market like this one: it fosters the perilous fallacy that a Thoroughbred foal is brought into the world to stand on a dais for a minute or two. For the good of the breed, ultimately we must reinforce the connection between commercial value and racetrack performance.

In the meantime, however, let's toast those hard-working and skilful people who have celebrated a bumper harvest. While the factory operations naturally headed the consignors' table by gross, the averages were again dominated by smaller outfits. All of us, scrolling down that list, will recognize names that warm the heart: friends, maybe kinsmen, lots of small farms that we admire.

Hats off to them, and also to those energetic and ambitious rivals, Keeneland and Fasig-Tipton, who have provided a trading environment equal to the current boom. Even if the cold winds out there soon come blasting through their pavilions, perhaps the next Flightline will meanwhile be getting to know the feel of a saddle on some dreamer's farm. Because we started with a person named Hope-and really that's every single one of us.

The post Depth Takes Market to Giddy Heights appeared first on TDN | Thoroughbred Daily News | Horse Racing News, Results and Video | Thoroughbred Breeding and Auctions.